PVTIME – Xinte Energy Co., Ltd. (01799.HK), a TBEA subsidiary that primarily produces and sells polysilicon, while also providing solar energy and wind power solutions, was listed on the main board of the Shanghai Stock Exchange on 19 September 2023. The company now appears to be engaging in intense competition with Tongwei and Daqo, two leading polysilicon manufacturers in the A share market, as well as GCL in the Hong Kong Stock market.

On the other hand, at the start of 2023, there was a significant drop in the prices of silicon materials. For instance, the price of dense polysilicon material decreased from its peak of 230/kg to 64 yuan/kg, resulting in a 72% decrease. When compared to the high point of 300 yuan/kg over the past two years, the drop was a massive 78.67%. This price decrease was critical for polysilicon manufacturers as the continuous low cost of silicon had caused a gradual reduction in their revenue and profits. The drop in silicon prices posed a significant challenge to the majority of silicon manufacturers from late 2020 to early 2021. Only five of the initial 20 global producers managed to withstand the tough shake-up.

How will the silicon manufacturers survive the current slump in silicon prices? And what are the major players planning for future development? This article compares the performance data of four major silicon material producers in China for the first half of the year, including revenue, net profits, production capacity, shipment volume, costs and innovation, to determine who will maintain their leading position.

Significant differences in incomes and profits

In the first half of 2023, China’s solar power capacity expanded by 78.42GW, showing a 153.95% year-on-year surge, as reported by the China National Energy Administration. The swift rise of photovoltaic installation boosted the performance of Chinese solar producers, with many attaining earnings growth in H1 2023. However, the silicon material producers had varying performances during the reporting period due to a significant decline in silicon material costs.

The top 4 silicon material producers in China were affected differently by the negative prices.

Tongwei generated the most revenue of 74.068 billion yuan in H1 2023, which increased by 22.75% due to their expansion of operations as reported by Tongwei. It made a profit of 13.27 billion yuan, showing an 8.56% rise, and was the only one of four firms to achieve increased net profits during H1 2023.

GCL’s earnings growth exceeds that of the other three silicon companies. As per its six-monthly report, GCL earned 20.946 billion yuan, an increase of 41.80%, with a net profit of 5.518 billion yuan, which dropped by 20.13%. The company stated that this is due to its steady expansion of granular silicon production and an increase in sales of polysilicon compared to the same period last year. GCL blamed the drop in its net profit on the considerable fall in prices of polysilicon.

Xinte Energy did not perform as well as the other three firms, both in terms of earnings and net profit. Its earnings went up by 19.51% to 17.587 billion yuan, whereas its net profit dipped by 15.28% to 4.759 billion yuan. The surge in earnings and the shifts in net profit were mostly due to the enhancement of polysilicon production capacity and higher sales of products. The report for the first half of 2023 shows that Xinte Energy sold significantly more polysilicon by about 80% compared to the previous year. The drop in polysilicon prices was the main reason for the decline in net profit, Xinte Energy stated.

Daqo did not perform as well as expected, and had a revenue of 9.234 billion yuan, a 42.93% decrease compared to the previous year. Net profit also decreased by 53.53% year on year, to 4.426 billion yuan. The poor results were caused by the significant drop in the price of polysilicon, which was due to the large amount of newly added production capacity in the silicon market, as reported by Daqo in its H1 2023 report.

Additionally, Director Zhang Longgen and General Manager Zhou Qiangmin had resigned following the release of the half-year report. Rumours suggested that their departure was linked to Daqo’s significant decline in performance.

Based on the H1 2023 data, the top four Chinese silicon companies differ in revenue and net profit. Tongwei demonstrated significant growth in both revenue and net profit, highlighting their proficiency. GCL’s significant increase in revenue was strongly connected to the need for granular silicon in the market. Compared to the other three corporations, Xinte Energy upheld a more steady record. Regrettably, Daqo was less successful than the other three companies when it came to revenue and net profit. This put Daqo at a disadvantage when comparing the other three firms. Daqo was the only company of the four solely involved in producing silicon materials, so it was bound to face tough times with the recent sharp drop in silicon prices. A critic expressed concern that Daqo could be the first of many in the silicon industry to crumble.

Upon examining revenue and net profit data, these four companies can be distinguished into three classifications. Tongwei takes the top position, whereas GCL and Xinte Energy rank in second place. Daqo, on the other hand, has fallen behind the first three companies as a whole.

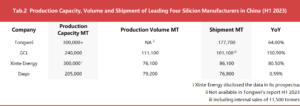

Different production capacity and shipment

During the first half of 2023, all producers in the industry recorded an increase in sales volume due to the substantial amount of new PV power additions in China. The four silicon makers also experienced the same growth in sales. In addition, as of the end of June 2023, the production capacities of these four makers were not significantly different.

Tongwei possessed a production capacity of more than 300,000 tonnes at the end of the reporting period. Xinte Energy did not disclose data on its production capacity, although it stated an annual capacity of 300,000 tonnes of high-purity polysilicon without a timeline. GCL had a capacity of 240,000 tonnes while Daqo projected a capacity of 205,000 tonnes per year by June 2023. As a result, Tongwei maintained its leading position with the largest production capacity among the four companies.

Tongwei did not disclose its production volume, while GCL generated 111,100 tonnes of silicon products in H1 2023, producing 82,400 tonnes of granular silicon, marking a considerable year-on-year surge of 634.3%. Xinte recorded production of 76,100 tonnes in H1 2023, a 3,000-tonne less than Daqo’s production volume of 79,200 tonnes.

Despite all companies experiencing positive growth in shipment volume in H1 2023, there was a notable disparity in their shipment data. Tongwei achieved shipments of 177,700 tonnes, which was a significant 64% increase from the same period of previous year. GCL secured the second position, thanks to its impressive shipments of granular silicon, totaling 101,100 tonnes, including internal sales of 11,500 tonnes. GCL recorded a remarkable year-on-year growth of 150.9%. Xinte Energy experienced a boost in its shipments, reaching 86,100 tonnes, reflecting an increase of 80.5% year-on-year due to the rapid upsurge in installed capacity. However, Daqo’s shipments of 76,800 tonnes only saw a 0.59% year-on-year increase, falling below the expected performance level.

Therefore, Tongwei excelled in terms of production capacity, as well as production and shipment volumes during H1 2023. The other three companies fell behind Tongwei in these areas, although the overall difference between these threes was minimal.

Different costs of top four silicon makers

Although Tongwei did not disclose its production costs, its sales price of 40,000 yuan per tonne, which was likely higher than its costs, was appealing. There were comments viewed Tongwei as crazy for innovating techniques to decrease its costs for polysilicon processing.

GCL has lowered their production costs for granular silicon in recent years. The quarterly report of April 2023 showed that the cost at the Leshan City location in China was 46,200 yuan per tonne. However, by July 2023, the cost had reduced to approximately 35,700 yuan per tonne at the same facility. GCL achieved up to a 22.73% decrease in cost through increased production capacity and processing optimization.

Daqo’s report for the first half of 2023 did not mention its production expenses. However, the firm mentioned that its use of electricity, water, and other types of energy was lower than the average amount disclosed by the China Photovoltaic Industry Association. This favourable situation, in terms of power usage and raw material consumption, should assist in cost-reduction efforts. It should be noted that Xinte is yet to update its production costs. As per their 2022 data, the production cost amounted to 68,600 yuan per tonne.

Based on 2022 data, the cost of producing one tonne of silicon material amounts to 68,600 yuan. Typically, major manufacturers spend around 40,000 to 60,000 yuan per tonne. However, second and third-tier companies face higher costs. Usually, their integrated cost of silicon material production ranges from 66,000 to 75,000 yuan per tonne (excluding tax). Manufacturers who provide similar silicon items with lower production expenses and prices will likely be preferred by clients and are predicted to uphold their place in the market as silicon prices keep decreasing.

Different R&D investment

The R&D investment of the four leading silicon companies in H1 2023 varied.

During the reporting period, GCL invested over 900 million yuan in research and development, representing a year-o-year increase of 30.9%. Besides granular silicon, it invested in self-developed CCZ technology, which shortens the crystal pulling process’s melting and other related processing time, boosting production efficiency and reducing costs. GCL’s crystal pulling furnace output surpassed 185kg/day per unit, while the pilot production line accomplished a capacity of 200MW.

Xinte Energy’s reduction in R&D investment was mainly caused by lower expenses in research and development during the reporting period, due to the late launch of most new projects by the group.

Daqo did not disclose the value of its R&D investment, but it outlined a series of upgrades to the core technologies. This includes a further reduction in energy consumption per unit of polysilicon through the use of energy recovery device and utilization technology. Additionally, it had decreased its emissions of recyclable chlorosilanes and other materials to close to zero by employing polysilicon material consumption control technology. The amount of metallic impurities and non-metallic carbon on the surface of crystalline silicon, as well as impurity content in donors and acceptors, which negatively impact the quality of polysilicon, were reduced using relevant technologies.

During their development, the four major silicon companies experience peaks and troughs. These silicon producers, as major suppliers within the industry chain, could encounter more challenging situations due to declining silicon prices and overcapacity. It remains to be seen if the rapid growth of the photovoltaic industry in China will boost the prospects of these makers.

Scan the QR code to follow PVTIME official account on Wechat for latest news on PV+ES

Scan the QR code to follow PVTIME official account on Wechat for latest news on PV+ES

, a TBEA subsidiary that primarily produces and sells polysilicon, while also providing solar energy and wind power solutions, was listed on the main board of…){kind=link}