PVTIME – In the opening quarter of 2026, the Chinese energy storage industry continued to grow strongly, driven by increasing demand in global markets. Chinese firms secured 52 firm energy storage orders in Q1 2026, excluding awarded tenders, representing a combined contracted capacity of 200GWh, a new quarterly record. This reflects the industry’s transition from policy-driven expansion to market-led, high-quality development, and reinforces the global competitiveness of China’s energy storage supply chain.

Global demand is being driven by three key forces: large-scale utility storage in Europe and the Americas; urgent energy infrastructure needs in the Middle East and Africa; and growing storage requirements linked to AI data centre operations. In China, the full implementation of capacity pricing has increased demand for renewable integration and grid peak-shaving services. Backed by advanced technologies such as large-format cells, liquid-cooled integration, and grid-forming controls, Chinese enterprises now cater to the generation-side, grid-side, customer-side, and export markets. They hold a global market share of over 60%, acting as a central pillar of the global energy transition. The volume of Q1 contracts underlines the widespread optimism and strong growth momentum across the value chain.

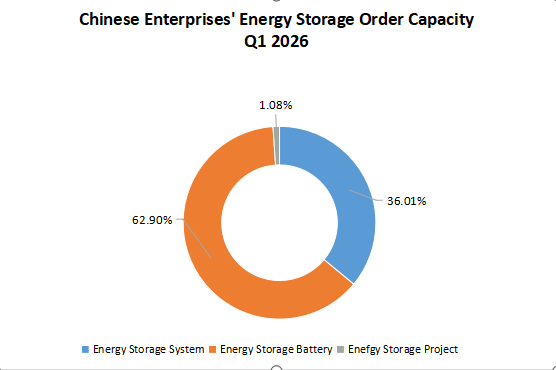

Order Structure Breakdown

The Q1 order portfolio has a clear structure centred on battery cells. This is supported by energy storage systems and complemented by full-scale project contracts. There are notable differences in scale and volume across the segments.

As the chart shows, the energy storage batteries and cells segment was the largest by capacity, accounting for 62.9% of the total. A total of ten contracts were signed in this category, amounting to 125.88GWh, with an average order size of over 13.99GWh. This reflects large-scale procurement linked to major renewable and storage bases, favouring high-capacity, high-energy-density cell solutions.

Energy storage systems were the most active segment in terms of transaction numbers, with 38 orders totalling 72.06GWh, equivalent to 36.01% of the overall contracted capacity. Strong demand spans residential, commercial, industrial, and grid-connected applications, with system integrators acting as a critical interface between upstream cell manufacturers and end users. A further three project-level orders totalling 2,160MWh and accounting for 1.08% of total capacity covered independent storage plants, grid-supporting facilities, and solar-storage hybrid developments. These represent the final stage of product deployment.

Regional market dynamics

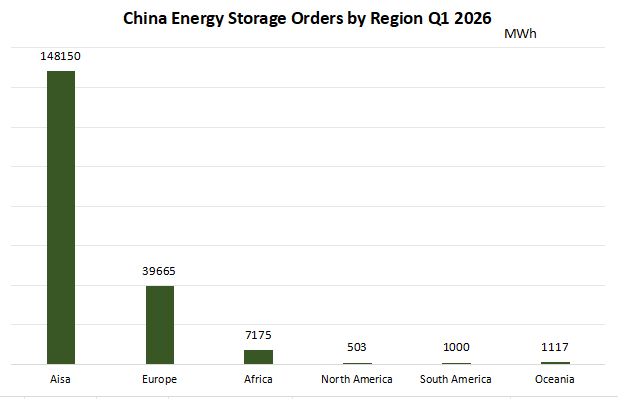

In Q1 2026, Chinese energy storage enterprises recorded global orders totalling 197.6GWh, thereby consolidating their leading international position.

Asia remains the dominant market, accounting for 75% of volumes. This is supported by accelerating renewable energy installations in Southeast Asia and the Middle East, as well as large-scale domestic projects. Europe is the second-largest market, with sustained opportunities for Chinese suppliers being created by strong policy support, resilient residential and commercial demand, and limited local manufacturing.

Collectively, Africa, Oceania, South America and North America account for less than 5% of order volumes, but offer targeted growth potential. Africa has seen significant activity related to large-scale renewable energy projects, while other regions are characterised by distributed and industrial-scale projects that support the global expansion of major Chinese companies.

Leading enterprise performance

More than 20 Chinese enterprises announced signed orders during the first quarter.

Against the backdrop of increasing renewable energy capacity and growing demand for grid balancing and frequency regulation, energy storage systems have evolved from optional extras to vital infrastructure. There was a surge in orders across utility-scale, commercial and industrial, and residential applications, which highlights the growing importance of the sector and the competitive dynamics among integrators.

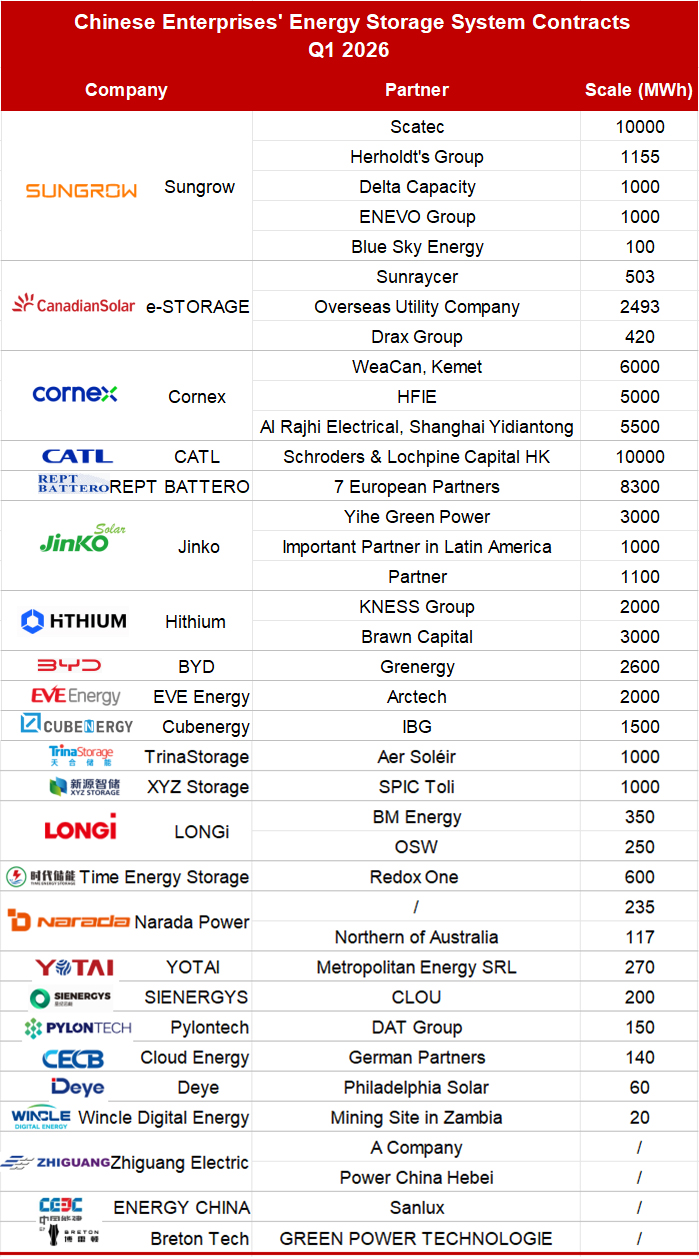

Highlight Transactions: Energy Storage Systems

Chinese firms secured contracts for more than 72.06GWh of energy storage systems in Q1 2026. Competition among leading integrators intensified, with large-scale orders becoming increasingly common. A total of 20 contracts exceeded 1GWh, accounting for 52.63% of all system-level transactions, while two contracts surpassed the 10GWh mark.

CATL and e-STORAGE were among the top performers, each securing a contract at the 10GWh scale. CATL signed a significant agreement with Schroder & Lochpine Capital HK, and e-STORAGE (Canadian Solar) collaborated with Scatec on a 10GWh project. These agreements highlight the increasing demand for multi-GWh-scale integrated storage solutions in global markets.

REPT Battero also secured a significant overseas contract, signing supply agreements with seven European partners at an international renewable energy exhibition in Italy. The deal covers 8.3GWh of energy storage systems to be delivered over two years, marking one of the largest multi-partner supply frameworks announced in the quarter.

Other notable transactions included Sungrow’s portfolio of contracts totalling over 3.2GWh with partners including Delta Capacity, ENEVO Group and Blue Sky Energy, reflecting its broad reach across multiple regional markets. Cornex New Energy also expanded its system-level footprint with contracts totalling over 11.5GWh with partners including WeaCan, Kemet and HFIE.

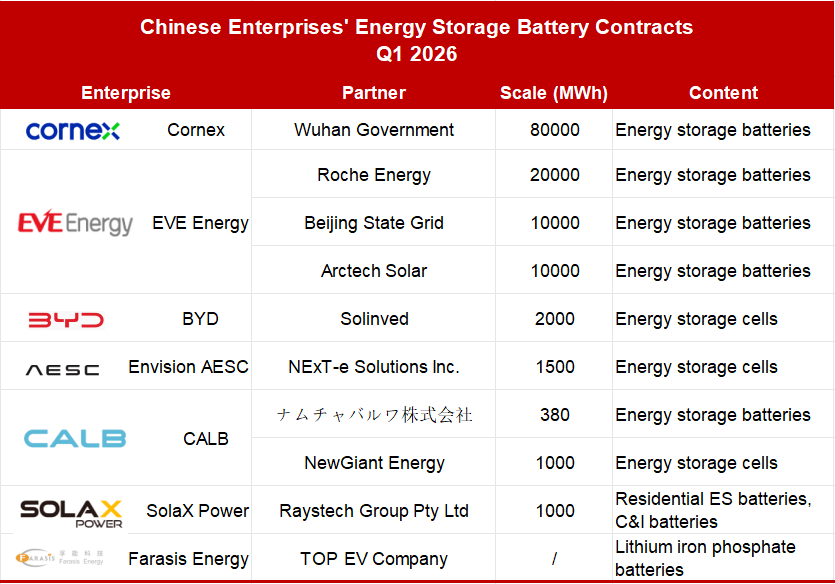

Highlight Transactions: Energy Storage Batteries and Cells

Demand for energy storage batteries and cells remained exceptionally strong globally in the first quarter of 2026, with leading Chinese manufacturers securing over 125.88GWh of contracted capacity. This accounted for 62.9% of the quarter’s total order volume, highlighting the importance of the upstream sector as the backbone of the energy storage supply chain. Not only have major players locked in large-scale orders, they have also advanced key strategic priorities, including high-capacity cell technology, international market expansion and long-term supply frameworks. This is steering the industry towards a new phase of high-quality growth.

Cornex New Energy secured the largest contract of the quarter by signing an investment agreement with the Wuhan Municipal Government for the second phase of its new energy battery production facility. The project has a planned annual capacity of 80GWh and will produce power batteries, energy storage cells and PACK modules. This agreement is a significant step in Cornex’s domestic expansion strategy, aimed at meeting the growing global demand for these products while also promoting local industrial development and economic growth in Wuhan.

EVE Energy also secured several high-profile contracts, including a three-year, 20GWh supply deal with Roche Energy. Half of this will consist of large-format cells with capacities of 628Ah and 588Ah, reflecting the industry’s shift towards higher-capacity designs. The firm also strengthened its domestic partnerships by signing a 10GWh strategic cooperation framework agreement with Beijing State Grid, with the aim of advancing grid-scale energy storage solutions.

Meanwhile, BYD continued to expand its international footprint by signing a 2000MWh energy storage cell supply agreement with Solinved, in support of solar and storage projects across Europe. Meanwhile, Envision AESC strengthened its position in the Japanese market through a three-year strategic procurement agreement with NExT-e Solutions Inc. , starting in 2026. The firm will supply 1,500MWh of dedicated energy storage cells to support system integration and project delivery in Japan and other global markets.

CALB made steady progress in Q1 with two key contracts. The first is a contract to supply 380MWh of energy storage batteries to Namchabarwa Co., Ltd. for projects in Japan. The second is a contract to supply 1,000MWh of cells to NewGiant Energy to support its downstream system development activities.

SolaX Power has expanded its presence in Australia through a 1,000MWh supply agreement with Raystech Group Pty Ltd. The contract covers residential and commercial and industrial energy storage batteries, reinforcing SolaX’s position as a leading provider of distributed storage solutions in the region.

Farasis Energy has also advanced its ambitions in the field of stationary storage through a partnership with a leading overseas new energy vehicle manufacturer. Although capacity details remain undisclosed, the agreement centres on lithium iron phosphate batteries for automotive and energy storage applications, showcasing the company’s increasing diversification beyond the EV sector.

Taken together, these transactions demonstrate the wide range of activity in China’s battery and cell sector. From large-scale domestic production projects to multi-year overseas supply frameworks, manufacturers are leveraging technological innovation and strategic partnerships to meet surging global demand, thereby consolidating their position as key players in the global energy transition.

The record-breaking performance in Q1 of 2026 underscores the robust growth of China’s energy storage industry, which has firmly established itself as a leader in cell, system, and project development technology. As global demand continues to rise, driven by the expansion of digital infrastructure and the push for decarbonisation worldwide, Chinese enterprises are well placed to extend their technological and commercial advantages. Further growth is anticipated in the upcoming quarters, driven by the deployment of large-scale projects and the ongoing international expansion of industry leaders.

Scan the QR code to follow PVTIME official account on Wechat for latest news on PV+ES

{kind=link}