PVTIME – The year 2025 was a pivotal period for China’s photovoltaic and energy storage sectors. The industry advanced in three key areas: large-scale capacity expansion, market-oriented operational reform, and optimisation of the global layout. This historic period saw significant growth in installed capacity, alongside profound restructuring of the industrial chain, divergent export performance, and global technological leadership.

Remarkable capacity leaps were achieved in both photovoltaic power generation and new energy storage, steadily decarbonising the national energy mix. While the photovoltaic industrial chain underwent structural adjustment, the energy storage segment emerged as the primary growth driver across the renewable energy sector.

Externally, export results revealed a polarised pattern, with subdued photovoltaic shipments and explosive growth in energy storage products. Domestic manufacturers actively tapped into emerging overseas markets and established local production bases to mitigate trade risks. Having shifted its strategic focus from blind capacity expansion to high-quality development, the sector has secured continuous core technological breakthroughs and deepened the integration of photovoltaic and energy storage systems. China has consolidated its dominant position within the global photovoltaic and energy storage landscape, driving the advancement of the worldwide green energy transition.

Historic Capacity Expansion Consolidates Global Leading Advantages

In 2025, China achieved two significant milestones in terms of the installed capacity of its photovoltaic and new energy storage facilities. Cumulative photovoltaic capacity exceeded one billion kilowatts, and new energy storage capacity surpassed one hundred million kilowatts. This further cemented China’s status as the world’s largest integrated renewable energy operator, setting a benchmark for global energy transition and carbon neutrality initiatives.

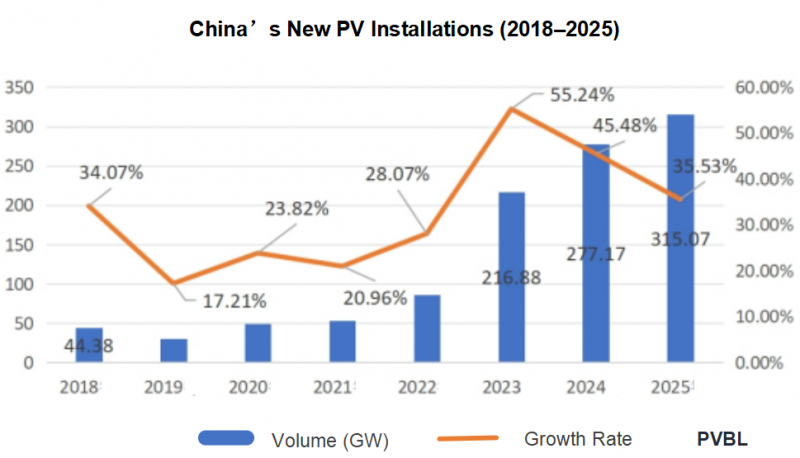

Official statistics released by the National Energy Administration showed that China added 315.07GW of new photovoltaic capacity in 2025. Building upon a substantial existing installed base, this strong growth increased the country’s cumulative photovoltaic capacity to 1201.73GW, representing a year-on-year increase of 35.53%, and marking the formal crossing of the one-billion-kilowatt threshold and the entry into a new development era. In parallel, new energy storage capacity expanded dramatically to reach the one hundred million kilowatt tier. The coordinated operation of photovoltaic power stations and energy storage facilities formed the world’s largest and most sophisticated integrated photovoltaic-storage energy infrastructure network.

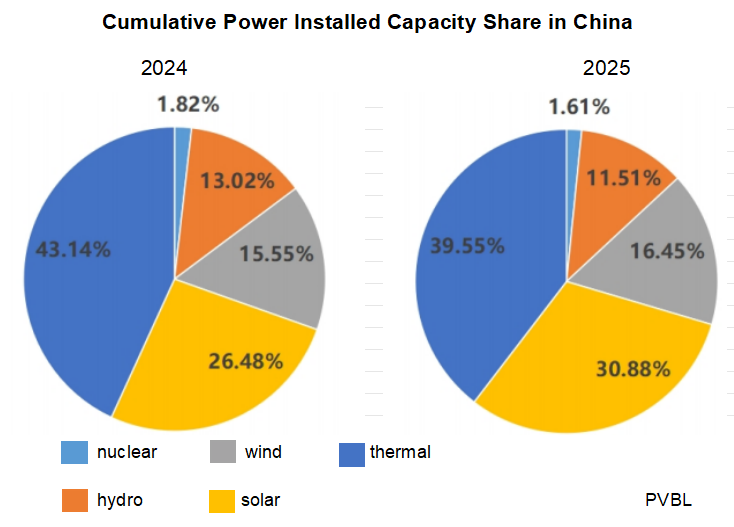

Comparative data on national power source capacity shares between 2024 and 2025 showed how wind and photovoltaic resources had reshaped China’s energy mix, gradually reducing the market share of thermal, hydropower, and nuclear generation facilities. In 2025, photovoltaic capacity accounted for 30.88% of the country’s total installed power capacity, up significantly from the 26.48% recorded in 2024. Meanwhile, thermal power’s proportion fell from 43.14% to 39.55%, dropping below the 40% threshold for the first time, which demonstrates tangible progress in reducing reliance on fossil fuels and achieving carbon emission reduction targets.

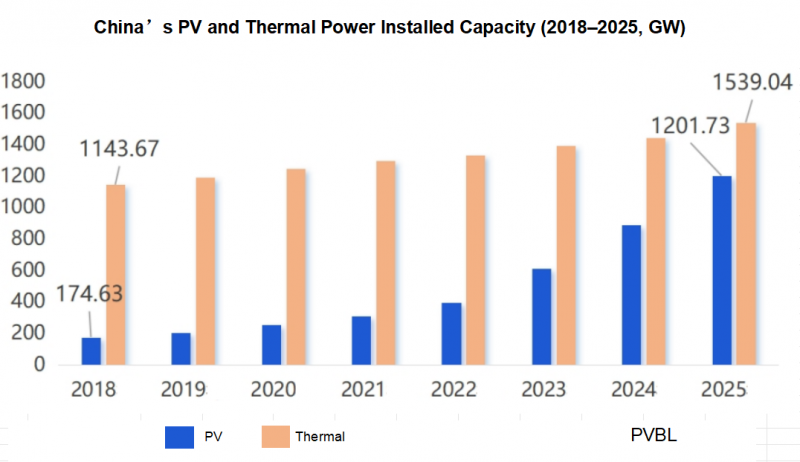

A retrospective review of China’s photovoltaic industry over the past eight years clearly shows its explosive growth trajectory and the narrowing capacity gap with thermal power assets. Data from the National Energy Administration showed that cumulative photovoltaic capacity stood at just 174.63GW in 2018, compared to 1,143.67GW of thermal power capacity, which equivalent to only 15.27% of thermal installations in the early stages of the large-scale rollout of renewable energy. While thermal power capacity grew steadily over the subsequent eight years, its expansion rate lagged far behind that of the photovoltaic sector. By 2025, China’s cumulative photovoltaic capacity had reached 1,201.73GW, representing an increase of 1,027.01GW since 2018, accounting for 78.08% of the country’s 1,539.04GW of installed thermal power capacity. This remarkable expansion highlights China’s world-leading pace in scaling up renewable energy. Combined with robust wind power capacity growth, wind and photovoltaic installations secured the highest global installed volume and market share. This established China as the nation making the fastest progress in energy transition and structural decarbonisation, while also spearheading the global green energy revolution.

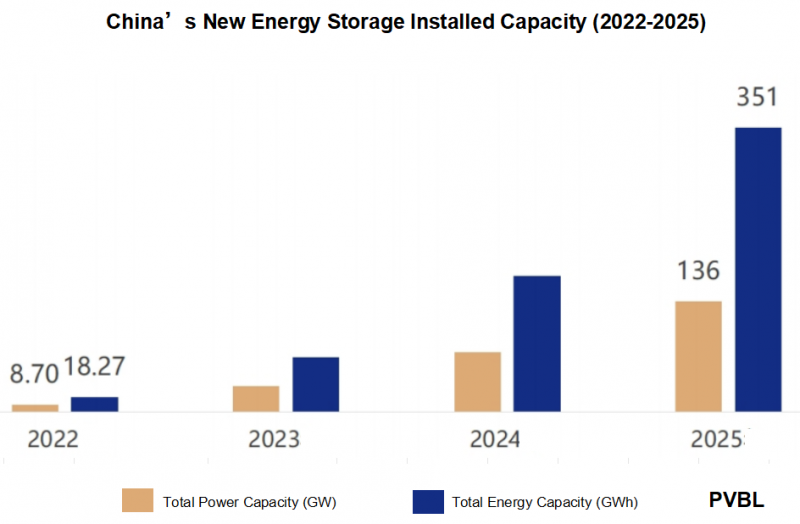

From 2022 to 2025, China’s new energy storage sector experienced spectacular exponential capacity growth. Official statistics showed that, during the initial industrial exploration phase, the country had a mere 8.7GW of cumulative power capacity and 18.27GWh of energy capacity for new energy storage in 2022. By 2025, installed power capacity had surged to 136GW, marking a 84% year-on-year increase from the 2024 year-end figure. Cumulative energy capacity reached 351GWh, with an average storage duration of 2.58 hours, a 0.30-hour improvement compared to the previous year-end figure. According to data compiled by the China Photovoltaic Industry Association, the total capacity of newly commissioned new energy storage in 2025 was approximately 62GW, paired with an energy volume of 183GWh. Within four years, power installation capacity had multiplied by over 15 times and energy capacity by over 18 times, marking a decisive shift from experimental deployment to large-scale commercial operation.

China’s new energy storage industry experienced extraordinary expansion due to coordinated policy guidance, technological efficiency upgrades, a robust industrial supply chain, increased market demand and a developed capital ecosystem. This phenomenal growth was underpinned by four pivotal development milestones: mandatory energy storage allocation requirements introduced in 2022; national strategic industrial upgrading in 2024; comprehensive market-oriented reform in 2025; and achieving global technological and manufacturing supremacy. Leading domestic enterprises, including CATL, BYD, EVE Energy and Great Power Energy & Technology, have built fully mature industrial chains covering battery cells, power conversion systems, battery management systems, and EPC services. These enterprises are continuously driving efficiency improvements and cost reductions. Meanwhile, system integrators such as Sungrow, HyperStrong, CRRC Zhuzhou Institute and Envision Energy have created a competitive, tiered industrial landscape with clear market segmentation, driving the rapid advancement of China’s domestic energy storage sector.

Structural Industrial Adjustment: Upstream contraction contrasts with downstream resilience and storage sector explosion

China’s photovoltaic industrial chain underwent clear structural differentiation in 2025. While upstream raw material output underwent periodic adjustment, the midstream and downstream segments sustained stable expansion, underpinned by steady market demand. According to official data from the China Photovoltaic Industry Association (CPIA), national polysilicon output totalled 1.34 million tonnes in 2025, marking a 26.4% year-on-year decline and the first annual decrease since 2013. Meanwhile, wafer production reached approximately 680GW, marking a 9.7% year-on-year decline and the first negative growth since 2009. This contraction in upstream output originated from historical capacity mismatches, intensified price competition, and short-term volatility in overseas market demand. Manufacturers implemented proactive inventory reduction and capacity optimisation strategies to stabilise product pricing and restore industrial profitability. Consequently, the upstream market faced a combination of high inventory levels and sluggish end-user demand during this transitional period.

The midstream and downstream photovoltaic segments demonstrated stronger operational resilience, with cell and module output maintaining positive growth. Domestic photovoltaic cell production exceeded 660GW in 2025, marking a modest year-on-year rise of 0.9%, while crystalline silicon module output surpassed 620GW, growing by 5.4%.

The energy storage segment has emerged as the core growth engine across the renewable energy industry, with domestic lithium-ion battery shipments for stationary storage applications experiencing explosive growth. Industry statistics predict that national storage lithium battery shipments will exceed 630GWh by 2025, reflecting an 85% year-on-year surge alongside rising market concentration among leading manufacturers. The three top suppliers CATL, which shipped over 140GWh; HiTHIUM and EVE Energy, which each delivered between 65 and 75GWh, jointly captured around 44% of the total market volume, thus consolidating their dominant competitive position.

Three primary factors fuelled the sharp rise in domestic storage battery demand. Firstly, the gradual withdrawal of compulsory storage allocation policies has facilitated the rapid grid connection of independent energy storage projects, driving the sector’s transition from passive, policy-driven deployment to market-led investment. Secondly, overseas market demand has rebounded strongly, driven by installation surges in North America, substantial order releases from emerging economies, and post-inventory correction growth in the global residential storage sector. Thirdly, the emergence of new application scenarios, including data centre backup power and commercial and industrial peak shaving, has generated continuous incremental demand for storage battery units.

The photovoltaic inverter market has grown steadily to meet domestic and international installation requirements, as well as supporting energy storage facilities. Research institutions in the industrial sector have projected that China’s inverter shipments will reach 336.7GW by 2025. Product iterations will prioritise string-type architectures, high-power ratings, and enhanced operational reliability.

China’s integrated photovoltaic-storage industrial chain has accelerated high-value upgrading through a dual development strategy involving domestic capacity optimisation and cross-border production localisation. Outdated, low-end domestic manufacturing capacity was phased out in order to allocate resources to breakthroughs in N-type photovoltaic technology, long-duration energy storage, and high-efficiency system integration. Meanwhile, leading manufacturers accelerated their global production layout to mitigate the risks posed by international trade barriers.

Optimised export structure: Sluggish PV shipments contrast with global storage market expansion.

By the end of 2025, China will hold 96% of global polysilicon capacity, 96.2% of wafer output, 91.3% of cell production and 80.1% of module manufacturing capacity, operating the world’s most resilient photovoltaic industrial ecosystem. The full-chain collaborative advantages, which span raw material supply, core equipment, advanced manufacturing and downstream system integration, have created unparalleled international competitiveness.

However, the year also saw a polarised export landscape, characterised by subdued photovoltaic commodity trade and exponential energy storage shipment growth. This was due to intensified cross-border trade barriers, domestic photovoltaic capacity imbalances, and the uneven progress of the global energy transition. China’s overseas expansion in the energy storage sector has achieved diversified regional growth, rather than relying on demand from a single market. Incomplete statistics compiled by the Energy Storage Application Branch of the China Electronics Standardisation Association recorded newly signed overseas orders and cooperative projects totalling 353GWh in 2025, marking a 94% year-on-year increase. Engineering, procurement and construction contracts, standalone storage systems and storage battery orders collectively reached 346GWh, representing a 90% year-on-year increase and highlighting the robust global market competitiveness of China’s energy storage industrial chain.

Electrochemical energy storage has evolved from an optional auxiliary facility to become an essential infrastructure asset. Photovoltaic-storage integrated solutions achieved worldwide market penetration in 2025, accounting for almost 90% of the global capacity of newly installed energy storage. Vertically integrated photovoltaic giants, including Trina Solar, JA Solar, Tongwei and LONGi, have strategically expanded their business portfolios into complementary energy storage sectors. Leveraging their comprehensive industrial expertise, advanced cost control capabilities, and well-established global distribution networks, these companies swiftly gained a foothold in the energy storage market. They did so by establishing proprietary brands, forming strategic partnerships, and making equity investments, all with the aim of delivering comprehensive smart energy solutions that cover system integration, core component research, and on-site project development.

This strategic industrial shift saw China’s leading photovoltaic manufacturers transform from global hardware suppliers into innovative system integrators and solution providers, driving the worldwide energy transition. Within the energy storage industry, companies replicated China’s proven large-scale manufacturing and rapid technological iteration models, reshaping global market competition patterns. Storage divisions acted as a secondary source of revenue growth, helping to stabilise corporate earnings amid cyclical industry fluctuations. Technological upgrades to battery cells, energy management systems, battery management systems and power conversion equipment delivered enhanced system performance and generated powerful operational synergies with photovoltaic manufacturing businesses. Photovoltaic assets provide abundant application scenarios and operational data optimisation experience for energy storage deployment. Meanwhile, storage technologies improve the dispatchability and economic value of solar power. Collectively, these factors strengthen enterprises’ global market competitiveness. Chinese energy storage enterprises are thus pivotal in advancing the industry from grid parity for standalone photovoltaic generation to integrated photovoltaic-storage grid parity.

Driven by global technological leadership, industrial competitiveness is being upgraded.

Backed by iterative technological innovation and mature full-chain advantages, Chinese photovoltaic and energy storage enterprises have retained global technological supremacy and are acting as core drivers of the worldwide transformation to renewable energy. The integrated photovoltaic-storage industrial sector has achieved dual leadership in technological advancement and market scale, thereby restructuring the competitive landscape of the global new energy industry.

Within the photovoltaic sector, domestic manufacturers have repeatedly set new world records for cell conversion efficiency, maintaining technological leadership across all mainstream technical routes. PERC technology has gradually entered mass production, while high-efficiency cell architectures, including TOPCon, HJT and BC, have achieved large-scale commercial deployment. Several vertically integrated companies have overcome mass-production bottlenecks for high-efficiency cells and are continuously breaking module efficiency benchmarks. BC-type modules developed by Aiko secured a certified commercial conversion efficiency of 24.8% under TAIYANG NEWS verification, with mass-produced product efficiency reportedly exceeding 25%. Silver-saving and silver-free metallisation technologies were widely adopted to mitigate cost pressures in the industry, while commercialised, gigawatt-scale production lines for perovskite photovoltaic technology developed by GCL enabled China to establish a dual-technology development framework combining high-efficiency crystalline silicon and next-generation thin-film photovoltaic solutions. This closed-loop domestic industrial chain offers unrivalled advantages in terms of technical performance, manufacturing stability, and cost control, enabling Chinese enterprises to drive the evolution of global photovoltaic technology.

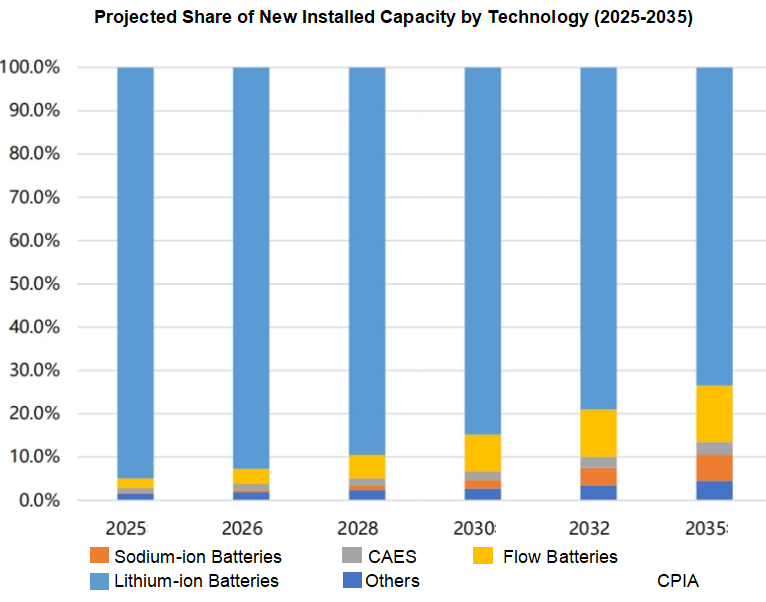

In the field of energy storage, breakthroughs in system integration and the development of core components have refined photovoltaic-storage-compatible technical architectures, ending reliance on imported key equipment. Domestic research has delivered advanced battery and energy management systems that can precisely monitor the operational status of cells and optimise energy scheduling. This enhances the safety and service lifespan of storage systems, while acting as the central operational control hub of integrated photovoltaic-storage facilities. Domestic high-power, high-efficiency power conversion systems have achieved world-leading grid adaptability and rapid response performance. Meanwhile, lithium iron phosphate storage cell manufacturing has matured alongside continuous cost declines. Emerging technologies, including sodium-ion and flow batteries, have entered large-scale pilot deployment in order to address limitations in long-duration and low-temperature operational scenarios. Chinese enterprises adopted a proven operational model combining bulk cell procurement, in-house core system development, and customised power conversion equipment adaptation. Leveraging their experience in the photovoltaic industry, these firms have achieved deep technological integration between photovoltaics and storage, delivering economically competitive, reliable, and scenario-adaptive integrated energy solutions.

In 2025, optimised export structures enabled Chinese enterprises to shift from volume-based hardware shipments to technology- and solution-oriented overseas expansion. Manufacturers diversified their market coverage across Latin America, Southeast Asia, the Middle East and Africa in order to avoid dependency on a single market, thereby securing record overseas order volumes. Domestic suppliers leveraged existing global distribution channels and brand recognition by bundling photovoltaic modules, energy storage systems and customised comprehensive energy solutions, thus expanding cross-border cooperation. Chinese integrated photovoltaic-storage solutions have become the preferred option for international renewable energy projects thanks to their superior power generation efficiency, competitive whole-life cycle costs, and customisable technical adaptability.

Scan the QR code to follow PVTIME official account on Wechat for latest news on PV+ES

{kind=link}