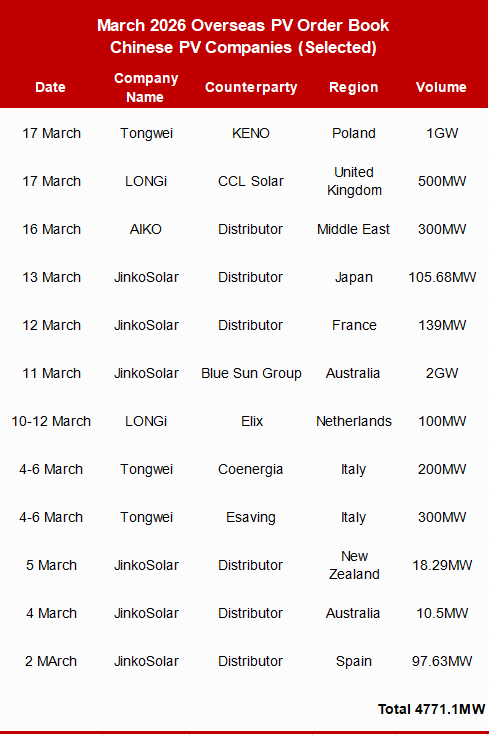

PVTIME – Global PV markets have witnessed a robust recovery in 2026, with component prices rebounding from early-year lows. According to industry data, March has emerged as a peak signing period for Chinese PV leaders, with four major firms securing a total of 4,771.1 MW in overseas orders between 2 and 17 March.

This surge dispels earlier concerns over overcapacity and weak demand, highlighting China’s dominant position in the global PV supply chain as firms utilise their entire industrial capabilities to secure significant market shares internationally.

The data reveals a highly concentrated pattern of orders, with JinkoSolar, Tongwei Solar, LONGi and AIKO accounting for the entirety of those recorded.

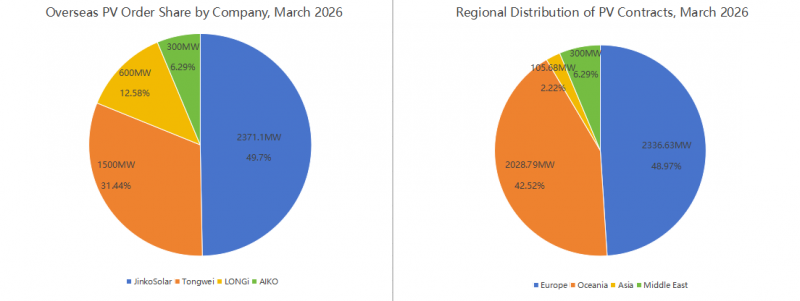

JinkoSolar led the way, securing six deals totalling 2,371.1MW, which equivalent to 49.7% of the total volume. These include a 97.63MW distributor contract in Spain on 2 March, a 10.5MW agreement in Australia on 4 March, an 18.29MW order in New Zealand on 5 March, a 2GW strategic cooperation memorandum with Australian distributor Blue Sun Group on 11 March, a 139MW contract in France on 12 March and a 105.68MW deal in Japan on 13 March. The 2GW agreement builds on over 1GW of cumulative deliveries between the two parties in the past three years and is regarded as one of the largest single orders in the industry’s history. It marks a milestone in the long-term collaborative partnerships between Chinese manufacturers and overseas distributors.

Tongwei follows with orders totalling 1,500MW, representing 31.44% of the total. Between 4 and 6 March, the firm signed modules agreements worth 300MW and 200MW with Italian partners Esaving and Coenergia, respectively, thereby strengthening its presence in southern Europe. On 17 March, Tongwei sealed a 1GW modules supply deal with KENO, Poland’s largest PV distributor. This extends the company’s reach into Central and Eastern Europe, a region which is experiencing rapid growth in renewable energy deployment.

Meanwhile, LONGi has secured 600MW in orders by focusing on high-end European markets: a 100MW contract with the Dutch firm Elix between 10 and 12 March and a 500MW BC module agreement with the UK-based CCL Solar on 17 March.

AIKO has expanded into emerging markets, signing a 300MW distributor order in the Middle East on 16 March and tapping into the region’s rapidly growing demand for green energy infrastructure.

Geographically, Europe remains the core market, absorbing 2,239MW, or 48.97%, of the total orders. Notable orders include Tongwei’s 500MW in Italy and 1GW in Poland, LONGi’s 100MW in the Netherlands and 500MW in the UK, and JinkoSolar’s 139MW in France. These orders reflect Europe’s urgent demand for energy independence, a legacy of past energy crises. Driven by policy frameworks such as the EU Clean Energy Package and the Carbon Border Adjustment Mechanism, European nations have increased their national PV installation targets in order to accelerate the transition away from fossil fuels. However, limited domestic PV manufacturing capacity has created a significant supply gap, making Chinese products the preferred choice for European buyers due to their cost-effectiveness and reliable, resilient supply chains.

The Asia-Pacific and Oceania markets accounted for 2,134.5MW, or 42.52%, of the total orders. JinkoSolar’s orders of 2,010.5MW in Australia, 18.29MW in New Zealand, and 105.68MW in Japan highlight the region’s diverse growth potential. Australia’s distributed order of 2GW underscores the strong demand for rooftop solar and distributed generation, while Japan’s contract demonstrates the market’s acceptance of high-efficiency modules that are tailored to the country’s strict technical standards. The Middle East is a key emerging market and has seen AIKO’s 300MW order. Oil-rich nations are accelerating their energy transition with large-scale green power and green hydrogen projects, which is positioning the region as the fastest-growing incremental market for Chinese PV exports.

Industry analysts have noted that the surge in orders in March aligns with broader first-quarter trends, with global PV contract volumes exceeding 200GW. Chinese firms secured 135GW, or 67.5% of the total, thus reinforcing their global leadership position. Unlike previous fragmented, small-scale orders, recent deals are large-scale and long-term, covering the supply of soler modules, the construction of power stations, the integration of energy storage and operational maintenance. This shift signals the evolution of Chinese PV firms from pure equipment exporters to comprehensive global new energy service providers, reflecting overseas market recognition of their technological and industrial strengths.

LONGi’s 500MW BC module order with CCL Solar exemplifies the growing importance of technological innovation in securing international contracts. Earlier, in February, the firm renewed a 2GW framework agreement with the European energy solutions provider Energy 3000, and secured 600MWh of energy storage systems and 100MW of high-efficiency modules with three key European partners at the Solar Solutions exhibition in Amsterdam. This further validates its BC technology as a preferred choice for European clients seeking high-performance, reliable solar solutions.

Despite the positive momentum, industry experts are cautioning against excessive optimism, stating that growth will be structural and of a high quality, rather than indiscriminate. The global transition to carbon neutrality provides a solid long-term foundation, with core markets such as Europe and the Middle East planning installations up to and beyond 2030. The decline in the levelised cost of electricity and the expansion of green power applications, ranging from residential rooftop systems to utility-scale solar farms, will support sustained growth. Meanwhile, large-scale GW orders will favour firms with comprehensive capabilities in production, technology, finance, and overseas operations. This trend will accelerate industry consolidation and the phasing out of inefficient capacity, promoting healthier, more sustainable development across the sector.

However, risks remain, including trade frictions, geopolitical volatility and exchange rate fluctuations, which may pose challenges to the overseas expansion of Chinese PV firms. Domestic capacity optimisation is essential to avoid over-expansion, rebalance supply and demand and prevent a return to the oversupply and price competition that characterised previous years. Future industry growth will focus on quality rather than quantity, and there will be no return to unregulated, disorderly expansion.

In conclusion, the 4,771.1MW order book for March represents a critical inflection point for the global PV industry. After years of overcapacity and margin pressure, the surge in overseas GW orders has utilised leading firms’ production capacity and secured their medium-to-long-term performance, breaking the cycle of destructive price competition that has plagued the sector.

While recovery is on the horizon, the market has not yet fully rebounded, with persistent risks such as trade barriers and incomplete capacity rationalisation. Industry divergence will intensify, with growth concentrated among top-tier players rather than across all firms. This is not a temporary boom, but rather the beginning of a new era of sustainable, high-quality growth for the global PV sector. This era will be driven by technological innovation, operational excellence, and long-term collaborative partnerships between Chinese PV giants and international clients.

Scan the QR code to follow PVTIME official account on Wechat for latest news on PV+ES

{kind=link}